Personal injury law – also known as tort law – protects people who are harmed by someone else’s actions or negligence. In a personal injury case, an injured person (the plaintiff) seeks compensation from the party who caused the harm (the defendant). Such injuries can include any harm to your body, mind, or emotions (as opposed to damage to property). This guide explains what counts as personal injury, how the legal claim process works, the role of attorneys and insurance, the types of damages you can claim, common insurance company challenges, statutes of limitations, and tips to maximize your settlement. Written in plain language, it will help accident victims understand their rights and options.

What Is “Personal Injury”? (Overview and Examples)

“Personal injury” covers a wide range of situations where one person is hurt due to another’s fault. Most personal injury cases are based on negligence – for example, a driver’s careless driving causing a crash, or a store owner’s failure to fix a hazard causing a slip and fall. They can also arise from intentional wrongs (like assault) or strict liability (such as a defectively made product causing injury).

Common examples of personal injury cases include:

- Auto Accidents: Car, truck, or motorcycle crashes caused by careless driving (the most typical personal injury scenario).

- Slip and Falls (Premises Liability): Injuries on someone’s property due to unsafe conditions (wet floors, broken stairs, ice, etc.).

- Medical Malpractice: Harm caused by a doctor’s or hospital’s negligence (surgical errors, misdiagnosis, medication mistakes).

- Product Liability: Injuries from defective or dangerous products (faulty appliances, unsafe drugs, etc.).

- Workplace Accidents: Injuries on the job (often handled via workers’ comp, but sometimes also personal injury claims if a third party was negligent).

- Intentional Torts: Assault, battery or other deliberate acts causing injury.

- Others: Dog bites, nursing home abuse, wrongful death (when an accident causes a fatality, the family can pursue a claim).

In sum, if you were physically or emotionally injured due to someone else’s negligence or wrongful act, it likely falls under personal injury law. Personal injury cases are civil (not criminal) actions – the goal is to recover money (“damages”) from the responsible party, not to convict them of a crime.

The Personal Injury Claim Process (Step by Step)

Filing a personal injury claim involves a series of steps from the time of the accident to resolution. While every case is unique, most follow a general timeline. Many cases settle out of court, and only about 5% of cases reach trial . Below is a flowchart of a typical personal injury claim process, followed by an explanation of each stage:

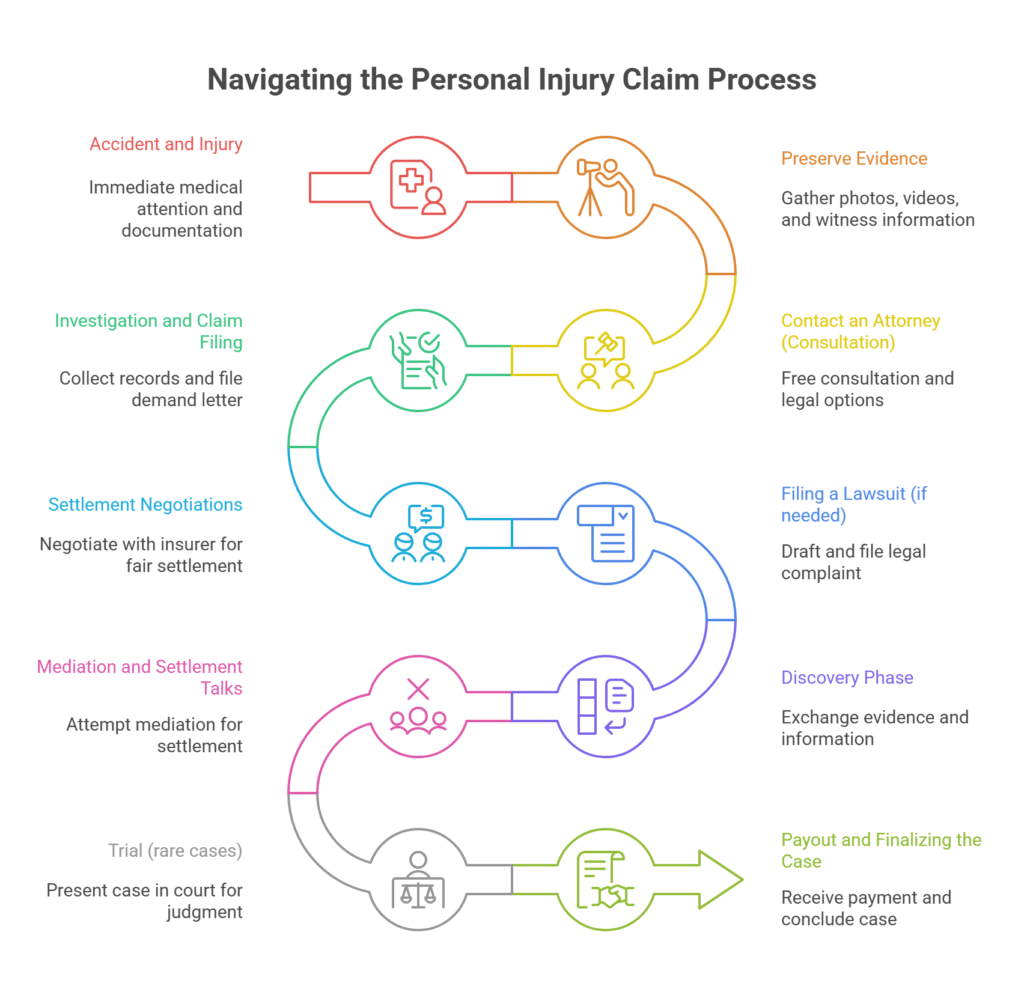

Personal injury claim process flowchart: from the initial incident and medical treatment through filing an insurance claim, legal proceedings, and resolution. Most cases begin with reporting the accident and seeking medical care, followed by consulting an attorney, investigating and gathering evidence, filing a claim or lawsuit, negotiation, and either settlement or trial.

1. Accident and Injury: The process starts with the incident that caused injury – e.g. a car accident, fall, or medical error. Your immediate priority should be health and safety: seek medical attention right away. Even if injuries seem minor, see a doctor – some injuries (like concussions or soft-tissue injuries) aren’t obvious until later . Prompt treatment creates medical records that document your injuries, which will be important evidence in your claim.

2. Preserve Evidence: If you are able, gather evidence at the scene. This includes photos or video of the accident scene, your injuries, property damage, hazard conditions, etc. Get contact information for any witnesses . If police respond (as in auto accidents), they will create an official police report, which is a key piece of evidence. In any accident, report it to the proper authorities (for example, call the police for a traffic crash or notify a manager for a store injury) so that an official report is on file . These reports provide an unbiased account of what happened.

3. Contact an Attorney (Consultation): It’s often wise to consult a personal injury attorney early. Most offer a free consultation and work on contingency fee (no upfront cost – more on this below). The attorney will hear what happened, evaluate if you have a valid claim, and explain your legal options. If you hire a lawyer, they will handle the legal legwork so you can focus on recovery. An experienced attorney will also immediately start protecting evidence and dealing with insurers on your behalf. (Note: If you plan to handle the claim yourself, you would instead notify the at-fault party’s insurance company of your claim, but be cautious giving statements – see Tips section.)

4. Investigation and Claim Filing: Your attorney (or you, if unrepresented) will conduct an investigation. This means collecting medical records, accident reports, witness statements, photos, and possibly expert opinions (e.g. an accident reconstruction or medical expert). The attorney will also determine all potential sources of recovery – for example, identifying all insurance policies that might cover the incident (auto insurance, homeowners or business liability insurance, etc. ). Once the evidence is gathered and you have a clear picture of your damages (the total losses from the injury), the attorney typically sends a demand letter to the at-fault party’s insurer. This demand letter outlines the facts of the case, the injuries and losses, and a proposed settlement amount. The insurer will review and respond.

5. Settlement Negotiations: After a demand letter, the insurance company may respond with a settlement offer or a denial. Usually, negotiations follow. Don’t be surprised if the insurer’s first offer is low – this is common (insurers often start with a “lowball” offer hoping you’ll settle cheap). Your attorney negotiates back and forth to reach a fair amount. Most personal injury claims are resolved through settlement at this stage, without going to court. This saves time and expense for all sides. However, if the insurer disputes liability or the two sides can’t agree on damages, the case may proceed to a lawsuit.

6. Filing a Lawsuit (if needed): When settlement talks stall or the insurer denies a valid claim, the next step is to file a civil lawsuit in court. Your attorney will draft a complaint (legal document outlining your allegations) and file it before the statute of limitations expires (see below on time limits). Once the lawsuit is filed and the defendants are served, the case enters the litigation phase. It’s important to note: filing a lawsuit doesn’t necessarily mean you’ll end up at trial. It often pressures the insurer to negotiate more seriously. In fact, even after a lawsuit is filed, settlement can occur at any time up to (or even during) trial.

7. Discovery Phase: After a lawsuit is filed, both sides engage in discovery, which is a formal exchange of evidence and information. Each side can send interrogatories (written questions), requests for documents, and take depositions (interviews under oath) of parties and witnesses. You may be asked to give a deposition, answer questions about the accident, and undergo an independent medical examination by a doctor hired by the defense. Discovery is a process to uncover all facts, which can take several months. During this phase, the defense may continue to try to deny or minimize your claim – for example, disputing the severity of your injuries or arguing some injuries were pre-existing. This is expected; your attorney will gather evidence to prove your case (medical reports, expert testimony, etc.) and counter the defense’s claims.

8. Mediation and Settlement Talks: Courts often require the parties to attempt mediation or a settlement conference before trial. Mediation is a meeting where a neutral mediator (often a retired judge or lawyer) helps both sides try to reach a voluntary settlement. The mediator doesn’t force a decision but facilitates negotiation. Many cases settle during or after mediation, as it provides a structured setting to bridge gaps. Settlement at this stage might involve the insurer agreeing to pay a sum and you signing a release of further claims. Most cases that reach this point do settle, since trials are risky and costly for both sides.

9. Trial (rare cases): If no settlement is reached, the case goes to trial. In a trial, your attorney presents your case to a judge or jury: witnesses testify, evidence is shown, and the defense presents their side. The judge or jury then decides if the defendant is liable and how much to award in damages. Trials can last anywhere from a day to several weeks in complex cases. Remember, trial is relatively uncommon – only a small percentage of personal injury lawsuits make it to a verdict . But it’s the stage where you can get a binding judgment if needed. If you win, the defendant (or their insurer) will be ordered to pay the award. If you lose, you get nothing (and potentially owe some legal costs). Either side can also appeal a trial result, which would extend the process further.

10. Payout and Finalizing the Case: When a settlement or verdict is reached, the final steps are about payment. In a settlement, the insurer typically must send the agreed payment within a short period (often 30 days) after paperwork is signed. In a trial verdict, if the plaintiff wins, the defendant’s insurer will pay the judgment up to their policy limits (if the verdict exceeds insurance coverage, collecting the excess from the defendant personally can be challenging). Sometimes additional steps occur, like resolving any liens (e.g. your health insurance or Medicare may claim reimbursement from your award for medical bills they covered ). Finally, your attorney will deduct their contingency fee and case costs, then you receive the net compensation. Most settlements are paid in a lump sum, while very large awards or certain structured settlements might be paid over time. The case is then concluded.

How long does all this take? It varies widely. A simple claim might settle in a few months, while a complex lawsuit could take a year or more (often 1–3 years) to reach resolution. Factors include the case complexity, the insurer’s willingness to settle, court schedules, etc. Patience is often required – but a thorough process usually yields a better outcome .

The Role of Attorneys and Contingency Fees

Do you need a lawyer for a personal injury case? While it’s not legally required, an experienced personal injury attorney can greatly benefit your case. Personal injury lawyers handle all the legal aspects: investigating the accident, gathering evidence, dealing with insurance adjusters, filing legal paperwork, negotiating settlements, and taking the case to trial if needed. This expertise often leads to higher compensation – studies have found that plaintiffs with legal representation receive settlements 3.5 times higher (on average) than those without.

Contingency Fee – “No Win, No Fee”: Most personal injury attorneys work on a contingency fee basis. This means you pay no upfront fees. The lawyer only gets paid if they recover money for you (through a settlement or verdict). The fee is typically a percentage of the amount recovered – commonly around 33% (one-third) of the recovery, though it can range (often 30–40%, and sometimes a bit higher if the case goes to trial or appeal). For example, if you settle for $90,000, a one-third contingency fee would be $30,000 to the attorney. If the attorney does not win any compensation for you, you owe them no fee. Contingency arrangements enable injured people to get legal help even if they can’t afford to pay a lawyer hourly. The exact percentage should be clearly stated in a written agreement you sign. Be aware that besides the attorney’s percentage, there may be case expenses (court filing fees, expert witness fees, etc.). Often the attorney will front these costs and then deduct them from the settlement at the end; your fee agreement should spell this out.

What a Personal Injury Lawyer Does: Your attorney’s job is to advocate for your best interests. Key roles of the lawyer include:

- Case Evaluation: Determining if you have a valid claim and whom to pursue (which parties are liable, what insurance applies).

- Legal Advice and Guidance: Explaining your rights, the legal process, and helping you make informed decisions (for example, whether to accept a settlement or sue).

- Investigation: Gathering evidence, interviewing witnesses, obtaining accident reports and medical records, possibly consulting experts – building the strongest case to prove the other party’s liability and the extent of your damages.

- Negotiation: Handling all communications with the insurance companies. Insurance adjusters are trained to save their company money – they might downplay your injuries or use anything you say against you. An attorney levels the playing field. They will prepare a compelling demand and negotiate for a fair settlement. Because the insurer knows the injured person has a lawyer ready to go to court, they often make a better offer than they would to an unrepresented person.

- Litigation: If a fair settlement cannot be reached, the attorney will file a lawsuit and represent you through the court process – drafting legal documents, arguing motions, taking depositions, and ultimately presenting the case at trial. This includes formulating legal strategy and countering the tactics the defense (or insurance lawyers) will use to diminish your claim.

- Maximizing Compensation: Perhaps most importantly, a good attorney will ensure you seek the full measure of damages available. It’s easy for a layperson to overlook categories of compensation (for example, future medical expenses or non-economic damages like pain and suffering). Lawyers have experience valuing claims and won’t leave money on the table. They also know what evidence is needed to prove less tangible losses. All of this contributes to getting you the maximum compensation you deserve.

Choosing an Attorney: If you decide to hire a lawyer, look for an experienced personal injury attorney with a good reputation. Many people choose a lawyer based on referrals or by researching online. Key factors might include: experience with your type of case (e.g. car accidents or medical malpractice), success record, whether they take cases to trial if needed (insurance companies may offer more if they know your lawyer is willing to go to court), and of course, someone who communicates well and makes you comfortable. During the initial consultation, you can ask about their fee (contingency percentage), any costs, and how they envision handling your case. Remember, you as the client have the final say on accepting a settlement or going to trial – the lawyer will advise, but decisions are ultimately yours.

In summary, while you can pursue a claim on your own, having a skilled attorney often pays for itself. They not only navigate the complex legal process and deal with the insurance company’s tricks, but also improve your odds of a higher payout to compensate you for all your losses. And with contingency fees, there’s little downside – if you recover nothing, you typically pay nothing.

Types of Damages You Can Claim (Economic, Non-Economic, Punitive)

When you file a personal injury claim, you are seeking “damages”, meaning monetary compensation for your losses. The law recognizes several categories of damages:

- Compensatory Damages: Intended to make the injured person “whole” for losses suffered. These break down into two sub-types: economic (special) damages and non-economic (general) damages .

- Punitive Damages: Intended to punish the wrongdoer for egregious conduct and deter others, rather than to compensate the victim. Punitive damages are not available in every case and are quite rare (only when the defendant’s actions were especially reckless or malicious) .

Below is a chart comparing these types of damages and examples of each:

| Type of Damage | Description & Examples |

|---|---|

| Economic Damages (Special Compensatory) | Tangible financial losses with a clear dollar value – medical bills, hospital stays, surgery costs, rehabilitation/therapy, medication, medical equipment; lost wages and income (including future earnings if you can’t work or have reduced earning capacity); property damage (for example, car repair/replacement in an auto accident); and other out-of-pocket expenses related to the injury (such as transportation to medical appointments, hiring help for household chores you can’t do, etc.) . These are calculated from bills, receipts, and pay stubs. |

| Non-Economic Damages (General Compensatory) | Intangible losses that don’t have an exact bill – the pain and suffering you’ve endured, both physical pain and emotional distress ; mental anguish or trauma (anxiety, depression, PTSD from the accident) ; loss of enjoyment of life (if your injuries hinder you from activities/hobbies you loved) ; loss of consortium (negative effects on your relationship with your spouse or family due to the injuries) ; and scarring or disfigurement (and its psychological impact) . These are real harms but harder to quantify. Often, lawyers use methods like a “multiplier” (multiplying the economic damages by a factor reflecting injury severity) or per diem (assigning a daily dollar amount to your pain) to estimate a reasonable amount . Supporting evidence like medical records, pain journals, and testimony can help prove these damages. Many states do not cap economic damages but some have caps on non-economic damages (especially in medical malpractice cases). |

| Punitive Damages | Punishment damages for when the defendant’s conduct was grossly negligent or intentional. Meant to punish and deter. For example, punitive damages might be considered if a drunk driver hit you, or a company knowingly sold a dangerously defective product. Punitive awards are not typical – they require a showing of willful or reckless disregard for safety. Many states have legal thresholds (e.g. needing “clear and convincing” evidence of fraud, malice, or willful wrongdoing) and some states cap punitive amounts. Punitive damages do not compensate losses but are added on top of compensatory damages if awarded . (In some states, a portion of punitive awards may go to the state). |

- mentation will make your lawyer’s job easier and your claim stronger.

- Be Careful with Insurance Adjusters: It’s usually you (or your lawyer) who will communicate with the insurance adjuster. Be truthful, but strategic. Do not admit fault (even polite apologies like “I’m sorry, I didn’t see you” can be misconstrued as admitting you caused the accident) . Stick to the facts of what happened and your injuries. If asked about your injuries early on, it’s okay to say you’re in pain and still undergoing evaluation, rather than stating specific limitations before you know the full diagnosis. Never give a recorded statement or sign any release for the opposing insurer without guidance. They might also ask you to sign a medical release to comb through your medical history – be cautious, as they often look for pre-existing conditions to pin your injuries on. It might be appropriate to sign a limited release for relevant records, but often your attorney will provide the needed records instead, to control what they see.

- Calculate All Your Damages (Don’t Settle Too Early): Before agreeing to any settlement, ensure it covers all your damages – past, present, and future. That includes future medical needs (will you need surgery or ongoing therapy? make sure those estimated costs are included) , lost future earning capacity (if you have a lasting injury that affects your ability to work or your career trajectory), and all the non-economic harm (pain, suffering, emotional distress) you endured . It can be hard to put a dollar on these, but consider how the injury impacted your life: Can you still do hobbies? Does it strain your family role? These intangible losses can be significant and should not be overlooked . If you settle too quickly, you might discover costs later that you can no longer claim . Tip: Wait until you reach Maximum Medical Improvement (MMI) – the point where you’ve either fully recovered or have a clear prognosis of any permanent effects – before settling, so you know the full extent of your injuries and necessary treatment.

- Don’t Rush to Accept the First Offer: As mentioned, initial offers are often low. Be patient and do not let financial pressure force you into a quick, inadequate settlement . It’s understandable that bills pile up after an accident, but if you can, use health insurance or other means in the short term while the claim is pending. If you settle fast for a low amount, you can’t go back for more later. Negotiation can take time, and sometimes filing a lawsuit is necessary to show you’re serious. Remember the saying: “Time is on the side of the one who’s willing to wait.” Insurance companies know that delaying can hurt you – but if you can endure and build a strong case, you often get a much better result.

- Keep Quiet on Social Media: In today’s digital age, insurance companies absolutely will monitor your social media. Anything you post publicly (and sometimes even privately) can potentially be used to argue your injuries aren’t that bad or that you’re not being truthful. For example, a photo of you smiling at a barbecue or a status update about a weekend trip can be taken out of context to “prove” you aren’t in pain or disabled, even if it was a brief moment of happiness or you were struggling during that activity. The safest approach is to avoid posting about your injury, your case, or any activities at all. Also, ask friends/family not to tag you in activities. Definitely do not rant about the other party or insurance online. It cannot help your case, it can only hurt. Maintain privacy while your claim is ongoing.

- Engage an Experienced Personal Injury Attorney: As discussed in the attorneys section – having a lawyer can significantly increase the value of your claim. They know how to value your case properly, negotiate effectively, and avoid the traps that insurance adjusters set. They also send a message to the insurer that you’re prepared to go the distance. If you’re worried about the cost – remember the contingency fee means no upfront payment, and lawyers typically don’t take cases unless they believe they can add value. Especially for serious injuries or when fault is contested, a lawyer’s expertise is invaluable. Tip: Hire an attorney early in the process.

Don’t wait until just before the statute runs or after you’ve made missteps. Early legal help can ensure all evidence is gathered and preserved, and that you avoid saying or doing things that could undermine your claim. It also relieves you of the stress of dealing with insurance calls and paperwork, which is worth it in itself.

Be Patient and Trust the Process: It’s natural to want a quick resolution, but as noted, patience can lead to a better outcome. Follow your attorney’s advice on when to push and when to wait. For example, rushing through medical treatment just to settle faster can harm your health and shortchange your claim. Let the medical process play out fully. Allow your attorney time to build a strong case and negotiate – settlements often happen right before a big milestone (like an impending trial date or mediation). If you abandon the process too soon, you leave money on the table. Lawsuits can be a slog, but that thoroughness usually pays off .

Don’t Underestimate Non-Economic Damages: People sometimes focus only on the stack of medical bills and lose sight of how much the injury has affected their life in non-monetary ways. Make sure to include claims for pain, suffering, and mental anguish if applicable . These can be a substantial part of your compensation in cases of severe injury or long-term consequences. Juries, especially, can be sympathetic to these human elements if presented well. Keep a diary of your daily pain levels, missed experiences, and emotional struggles – this can be powerful evidence. Discuss with your attorney all the ways the injury changed your life so they can pursue those damages. Don’t feel shy to seek compensation for these just because they’re hard to quantify – they are a recognized part of the law.

By following these tips, you help maximize the strength and value of your personal injury claim. To illustrate, consider an example: Suppose you’re in a car accident. You promptly call 911 and get medical help (documented injuries), take photos of the scene, and exchange info with witnesses (evidence). You follow up with your doctor and physical therapy for months (establishing the extent of injuries). You keep a journal of how the pain affects your daily life (proof of suffering). When the insurance adjuster calls, you give a brief statement of facts and decline to go on record or accept the quick $3,000 offer they make. You consult a reputable injury attorney, who values your case at $50,000 because of a herniated disk and several months of lost work. Your attorney negotiates, leveraging all your documentation, and is willing to file suit. After some back-and-forth – perhaps even mediation – the insurer agrees to pay $40,000. Because you were proactive and patient, you avoided settling for $3k and obtained a far more just outcome.

Finally, remember that every case is different. There’s no guaranteed formula for success, but being informed and prepared tilts the odds in your favor. If at any point you feel overwhelmed, don’t hesitate to seek professional legal advice. An attorney can provide personalized guidance and handle the heavy lifting, which in itself can bring peace of mind during a tough time.

Conclusion: Suffering a personal injury can be life-changing – physically, emotionally, and financially. But the civil justice system provides a way for you to seek compensation and hold the responsible party accountable. We’ve covered the essentials: from understanding what qualifies as personal injury, to navigating the legal claim process with the help of contingency-fee attorneys, to dealing with insurance and knowing what damages you can claim. By being proactive, organized, and informed (and with skilled legal support when needed), you can level the playing field against insurance companies and maximize your chances of a fair settlement or verdict. Keep these insights and tips in mind as you pursue your personal injury claim. While the process may be challenging, it is fundamentally about getting you the resources and justice you need to recover and move forward with your life . Good luck, stay safe, and don’t hesitate to seek out the support you deserve on the road to recovery.

Sources:

American Bar Association – Definition of Personal Injury/Tort

Cornell Law School Legal Information Institute (Wex) – Personal Injury overview

GJEL Accident Attorneys – Personal Injury Case Timeline/Flowchart

Dan Christensen, TeamJustice (DJC Law) – Personal Injury Lawsuit Timeline (2025)

James Morris Law – Insurance Company Tactics

Express Legal Funding – Insurance “Delay, Deny, Defend” Strategy (2025)

Resmini Law Offices – Economic vs. Non-Economic Damages Explained (2024)

Enjuris (Personal Injury Compensation Guide) – Compensatory vs. Punitive Damages

Cellino Law – Insurance Policy Limits in Injury Claims (2024)

The Simon Law Group – 10 Tips to Maximize Personal Injury Compensation (2024)